Selected Macroeconomic Factors & Indicators Pertinent to Bay Area Real Estate Markets

Interest rates, financial markets, inflation, housing affordability, consumer confidence, employment, population change, mortgage debt, and other factors and indicators.

Good-faith illustrations of data provided by sources deemed reliable, but may contain errors and subject to revision. Some of these indicators are highly volatile and can change significantly even over the short term. All numbers should be considered approximate, and subject to independent verification by interested parties.

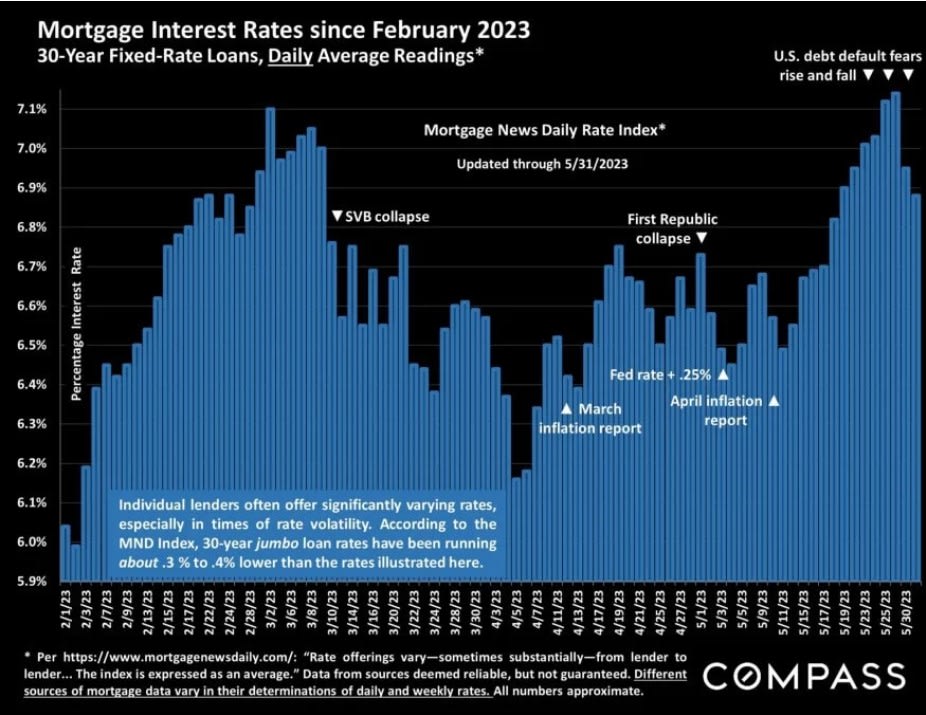

Mortgage Interest Rates since February 2023

30-Year Fixed Rate Loans, Daily Average Readings*

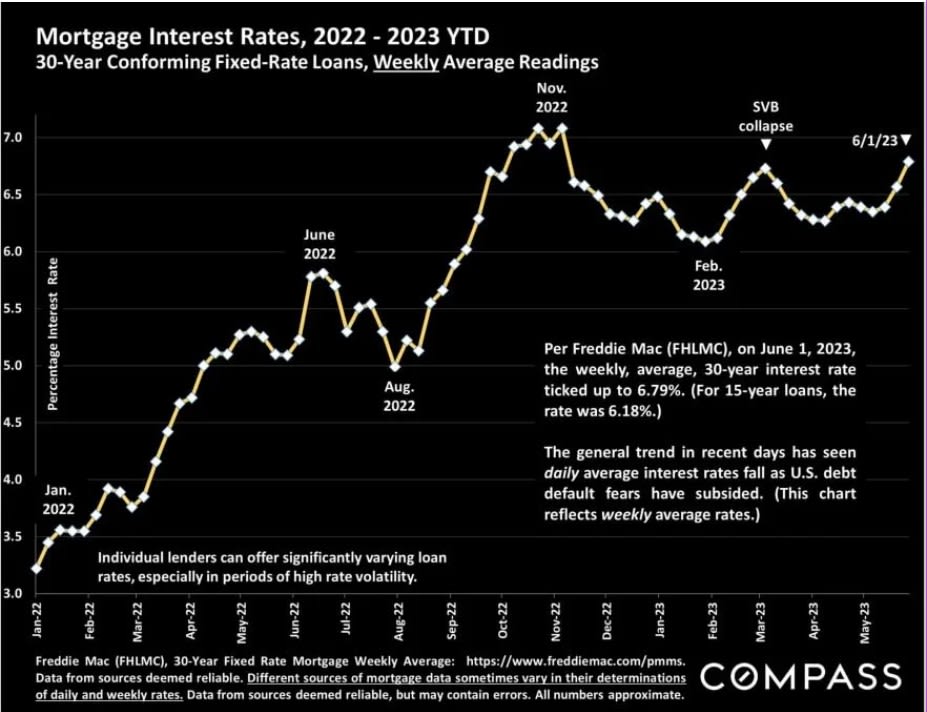

Mortgage Interest Rates, 2022-2023 YTD

30-Year Conforming Fixed-Rate Loans, Weekly Average Readings

Per Freddie Mac (FHLMC), on June 1, 2023, the weekly, average, 30-year interest rate ticked up to 6.79%. (For 15-year loans, the rate was 6.18%.)

The general trend in recent days has seen daily average interest rates fall as U.S. debt default fears have subsided. (This chart reflects weekly average rates.)

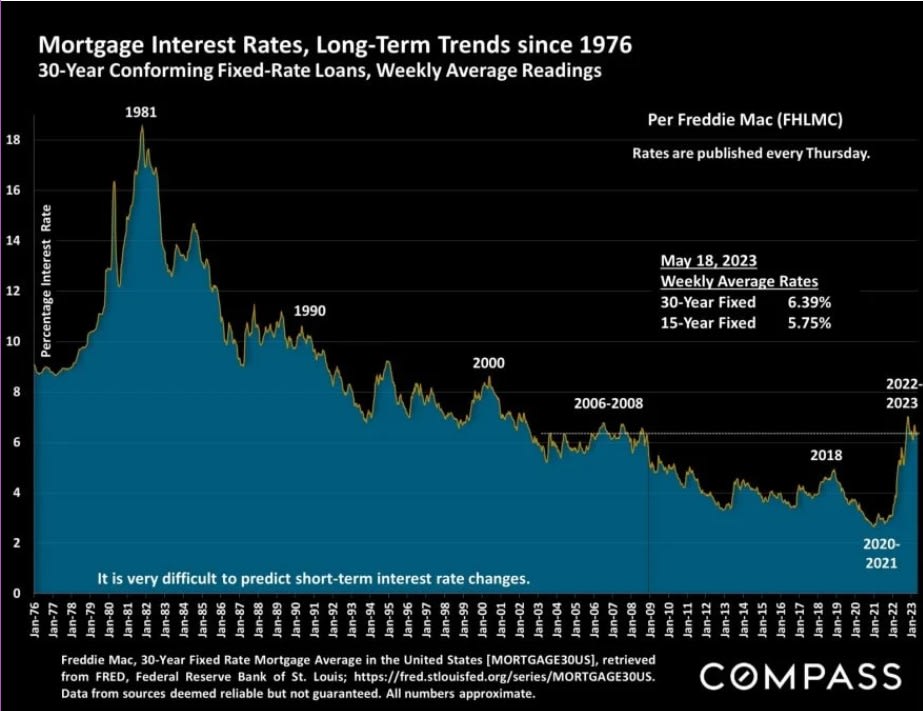

Mortgage Interest Rates, Long-Term Trends since 1976

30-Year Conforming Fixed-Rate Loans, Weekly Average Readings

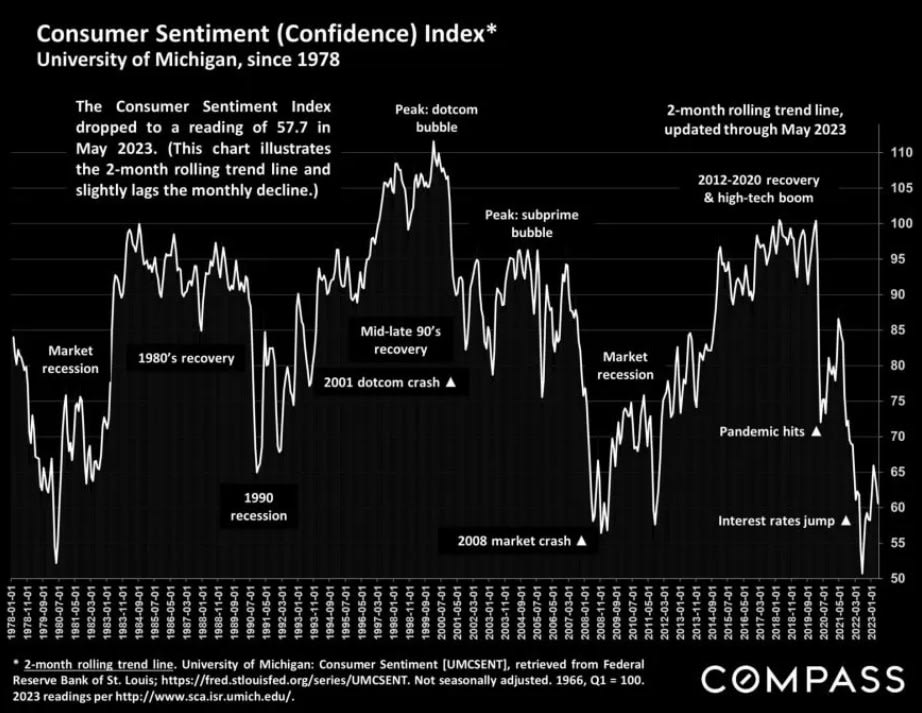

Consumer Sentiment (Confidence) Index*

University of Michigan, since 1978

The Consumer Sentiment Index dropped to a reading of 57.7 in May 2023. (This chart illustrates the 2-month rolling trend line and slightly lags the monthly decline.)

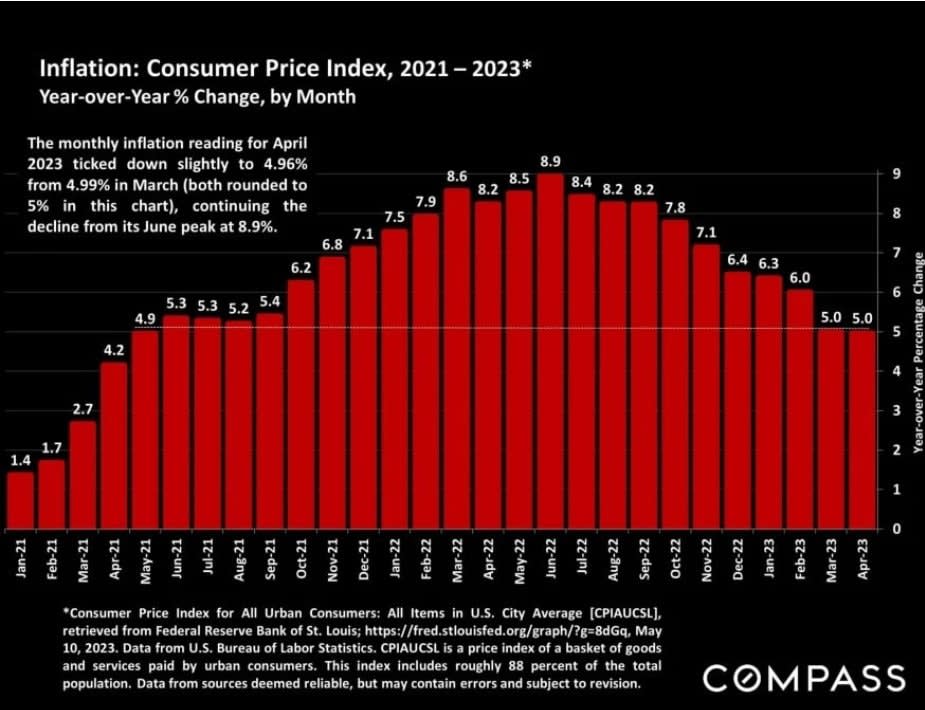

Inflation: Consumer Price Index, 2021 - 2023*

Year-over-Year % Change, by Month

The monthly inflation reading for April 2023 ticked down slightly to 4.96% from 4.99% in March (both rounded to 5% in this chart), continuing the decline from its June peak at 8.9%.

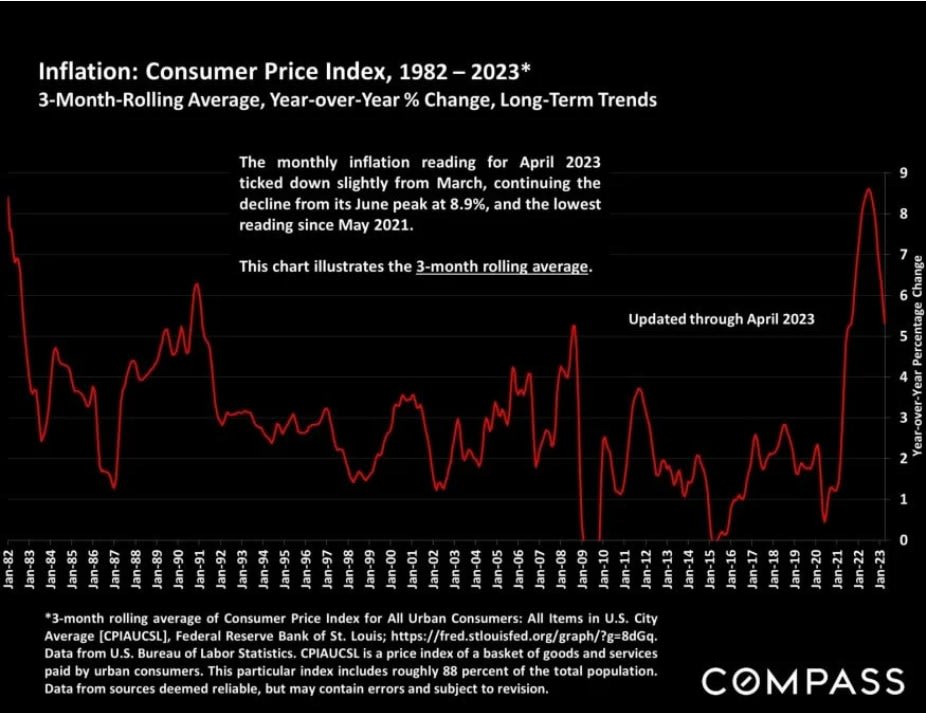

Inflation: Consumer Price Index, 1982-2023*

3-Month-Rolling Average, Year-over-Year % Change, Long-Term Trends

The monthly inflation reading for April 2023 ticked down slightly from March, continuing the decline from its June peak at 8.9%, and the lowest reading since May 2021.

This chart illustrates the 3-month rolling average.

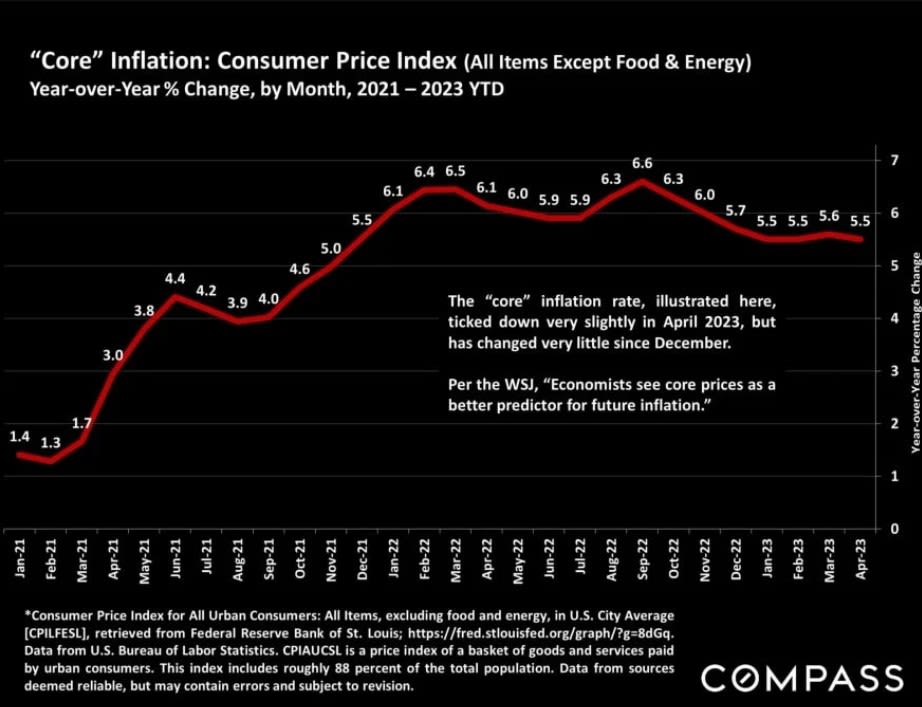

"Core" Inflation: Consumer Price Index (All Items Except Food & Energy)

Year-over-Year % Change, by Month, 2021-2023 YTD

The "core" inflation rate, illustrated here, ticked down very slightly in April 2023, but has changed very little since December.

Per the WSJ, "Economists see core prices as a better predictor for future inflation."

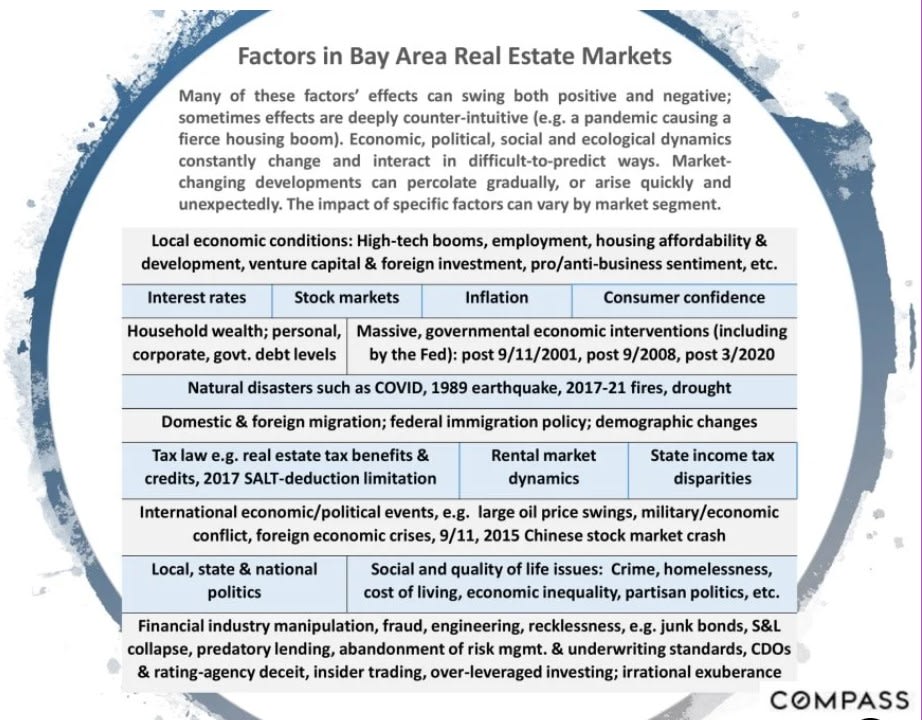

Factors in Bay Area Real Estate Markets

Many of these factors' effects can swing both positive and negative; sometimes effects are deeply counter-intuitive (e.g. a pandemic causing a fierce housing boom). Economic, political, social and ecological dynamics constantly change and interact in difficult-to-predict ways. Market-changing developments can percolate gradually, or arise quickly and unexpectedly. The impact of specific factors can vary by market segment.

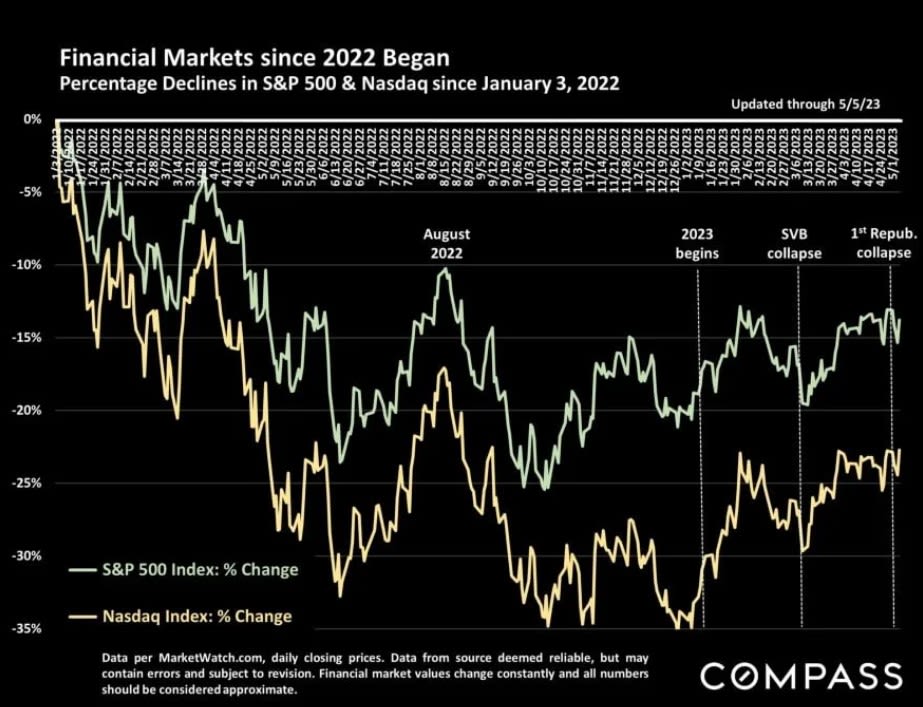

Financial Markets since 2022 Began

Percentage Declines in S&P 500 & Nasdaq since January 3, 2022

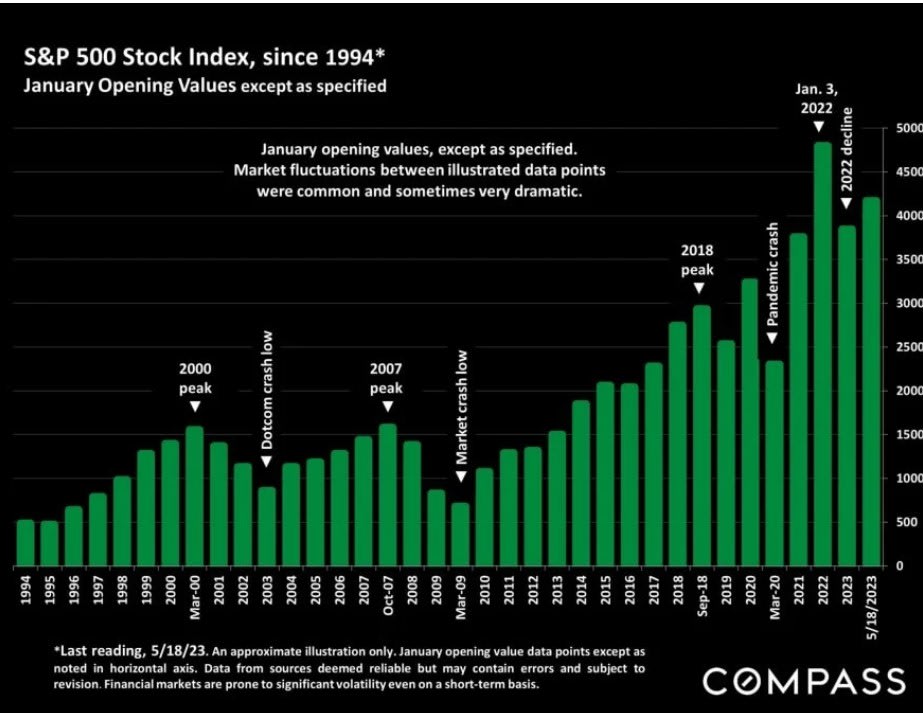

S&P 500 Stock Index, since 1994*

January Opening Values except as specified

January opening values, except as specified. Market fluctuations between illustrated data points were common and sometimes very dramatic.

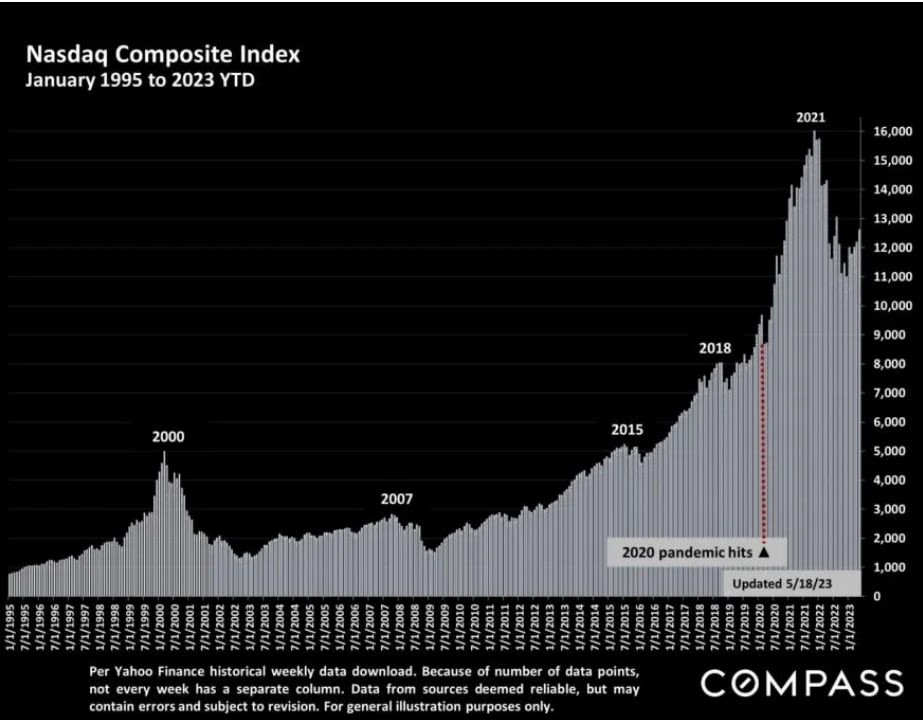

Nasdaq Composite Index

January 1995 to 2023 YTD

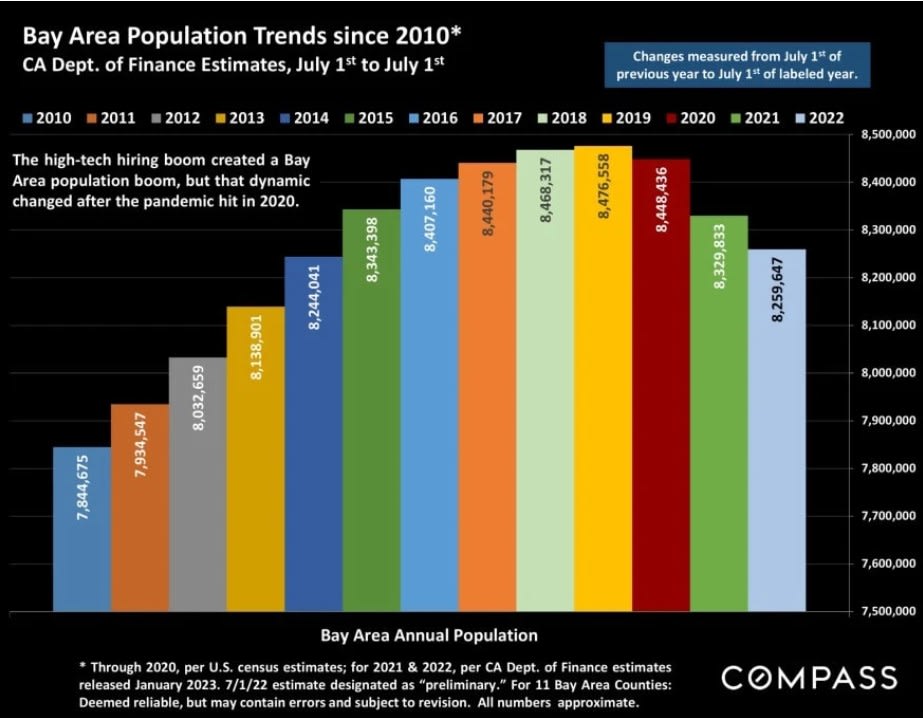

Bay Area Population Trends since 2010*

CA Dept. of Finance Estimates, July 1st to July 1st

Changes measured from July 1ST of previous year to July 1st of labeled year.

The high-tech hiring boom created a Bay Area population boom, but that dynamic changed after the pandemic hit in 2020.

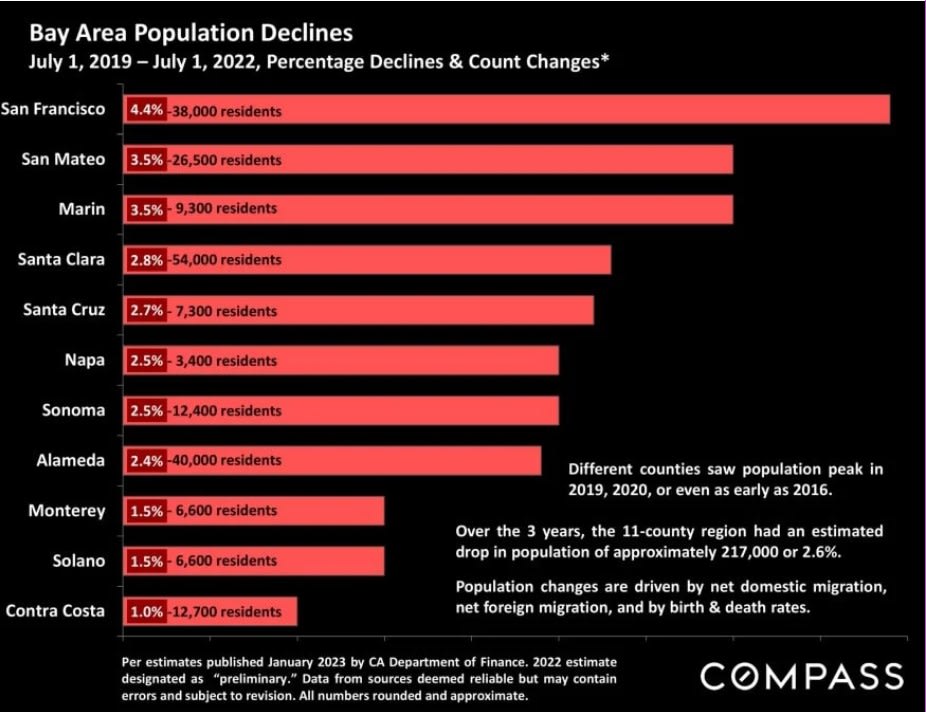

Bay Area Population Declines

July 1, 2019 - July 1, 2022, Percentage Declines & Count Changes*

Different counties saw population peak in 2019, 2020, or even as early as 2016.

Over the 3 years, the 11-county region had an estimated drop in population of approximately 217,000 or 2.6%.

Population changes are driven by net domestic migration, net foreign migration and by birth & death rates.

Summary Points about Migration & Population Changes

Most people moving out-of-county in the Bay Area move to an adjacent county (often to more affordable, less densely populated counties), or to the circle of even more affordable CA counties outside the Bay Area. (There has also been significant, recent migration to other areas such as Lake Tahoe and San Diego.) Within the Bay Area, the general direction is from more expensive housing locations to more affordable markets (but there are many exceptions).

Since the pandemic struck, migration and population changes often played out differently between homeowners of varying types (house, condo, etc.), tenants, and university students (as schools closed and reopened), with differing effects on county housing markets. The pandemic also had some significant effects, presumably temporary, on birth and death rates.

Per U.S. Census data, when moving out of state, Bay Area and CA residents mostly choose states with no state income tax (Texas, Nevada, Washington, Florida), other adjacent states (Arizona, with a much lower state income tax rate, and Oregon) and/or states with major high-tech centers (Texas, Washington). Colorado is also typically in the top 7. All of which have lower housing costs. CA has the highest state income taxes for affluent residents in the country.

People moving into the Bay Area come from everywhere - including a very significant number coming from foreign countries. Even as domestic migration rates have turned negative in recent years, foreign immigration rates have typically stayed positive after plunging in the immediate aftermath of the pandemic hitting) .

There is often a lot of 2-way traffic between locations: for example, between Bay Area counties; between SoCal or New York and the Bay Area; between Texas or Washington and California. Hundreds of thousands of residents move within, into and out of the Bay Area every year.

There are many volatile economic and demographic factors still at play, and how they will affect migration and population in coming years is unknown.

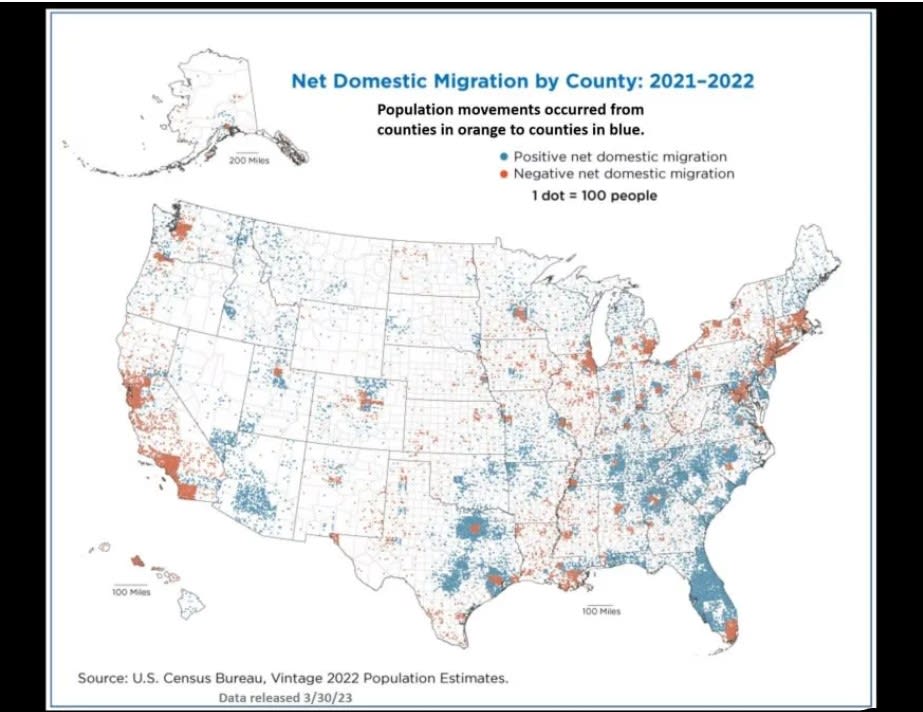

Net Domestic Migration by County: 2021-2022

Population movements occurred from counties in orange to counties in blue.

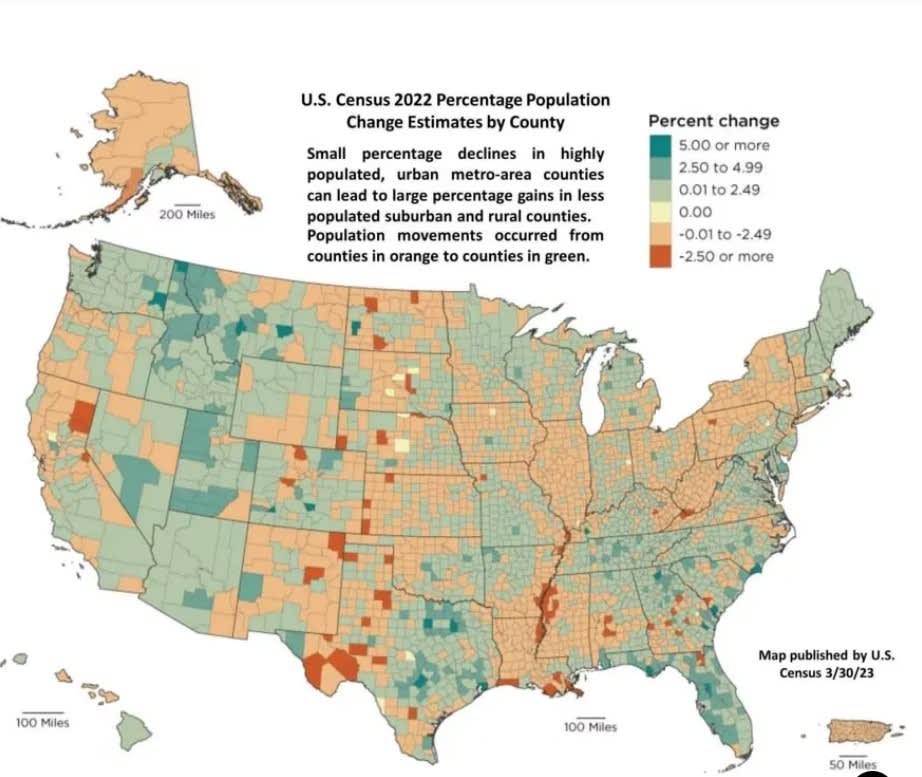

U.S. Census 2022 Percentage Population Change Estimates by County

Small percentage declines in highly populated, urban metro-area counties can lead to large percentage gains in less populated suburban and rural counties. Population movements occurred from counties in orange to counties in green.

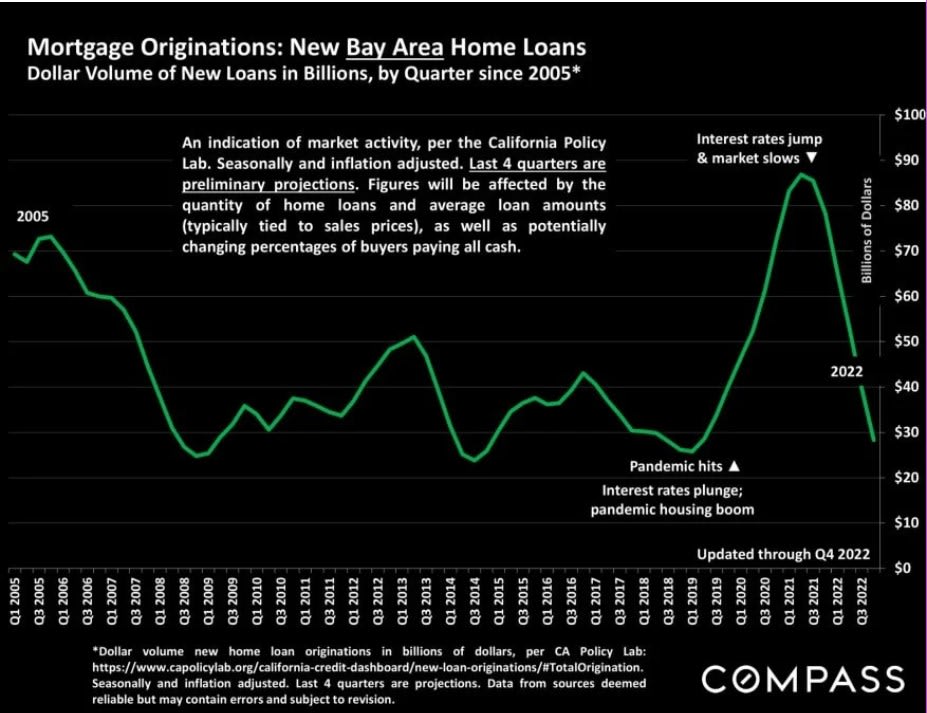

Mortgage Originations: New Bay Area Home Loans

Dollar Volume of New Loans in Billions, by Quarter since 2005*

An Indication of market activity, per the California Policy Lab. Seasonally and inflation adjusted. Last 4 quarters are preliminary projections. Figures will be affected by the quantity of home loans and average loan amounts (typically tied to sales prices), as well as potentially changing percentages of buyers paying all cash.

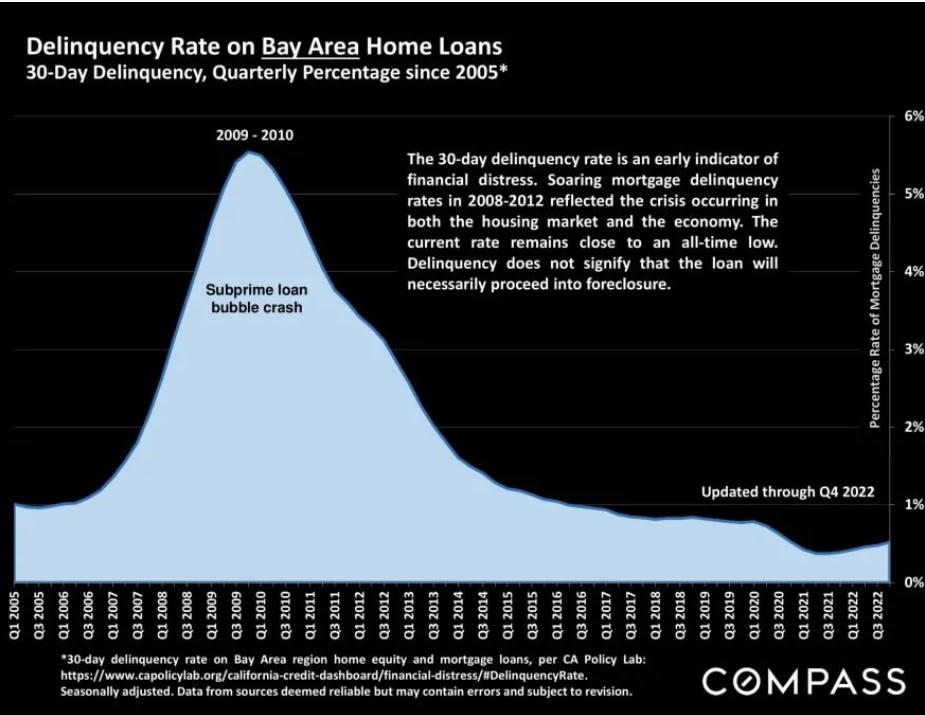

Delinquency Rate on Rate on Bay Area Home Loans

30-Day Delinquency, Quarterly Percentage since 2005*

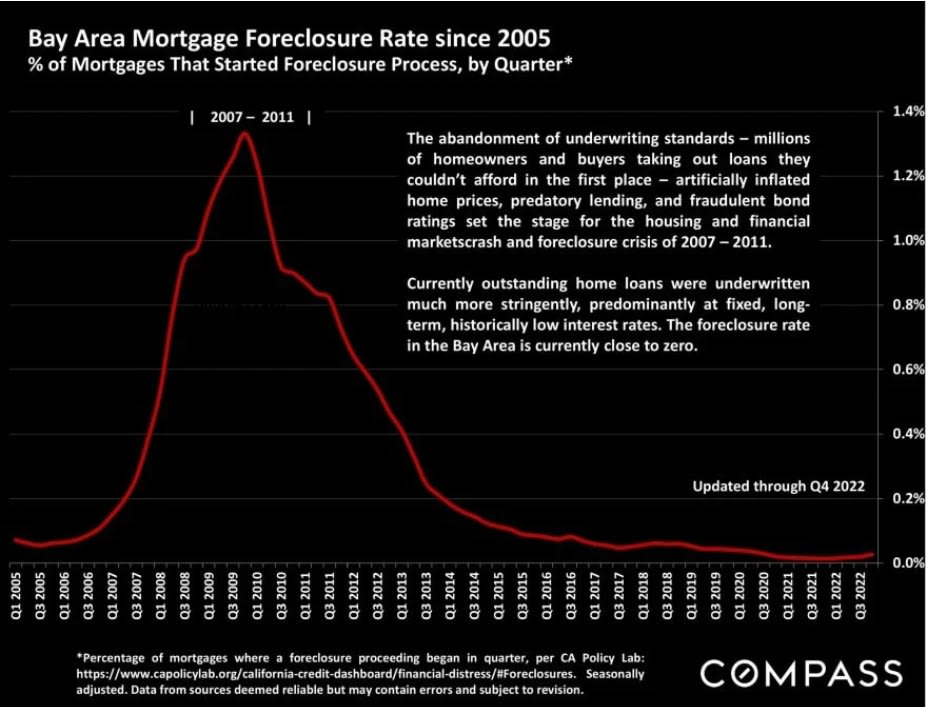

Bay Area Mortgage Foreclosure Rate since 2005

% of Mortgages That Started Foreclosure Process, by Quarter*

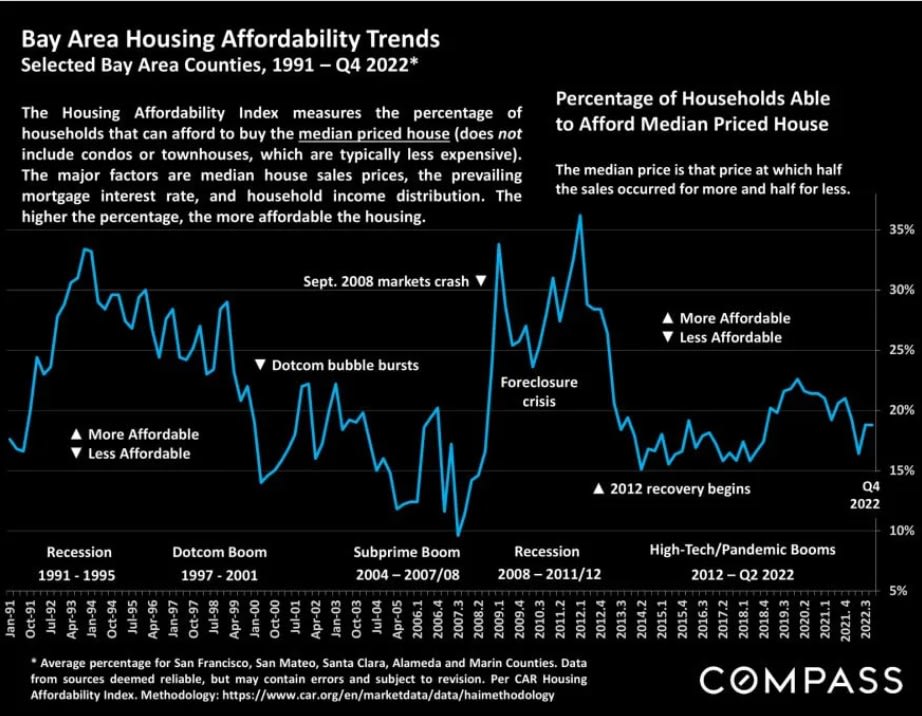

Bay Area Housing Affordability Trends

Selected Bay Area Counties, 1991- Q4 2022*

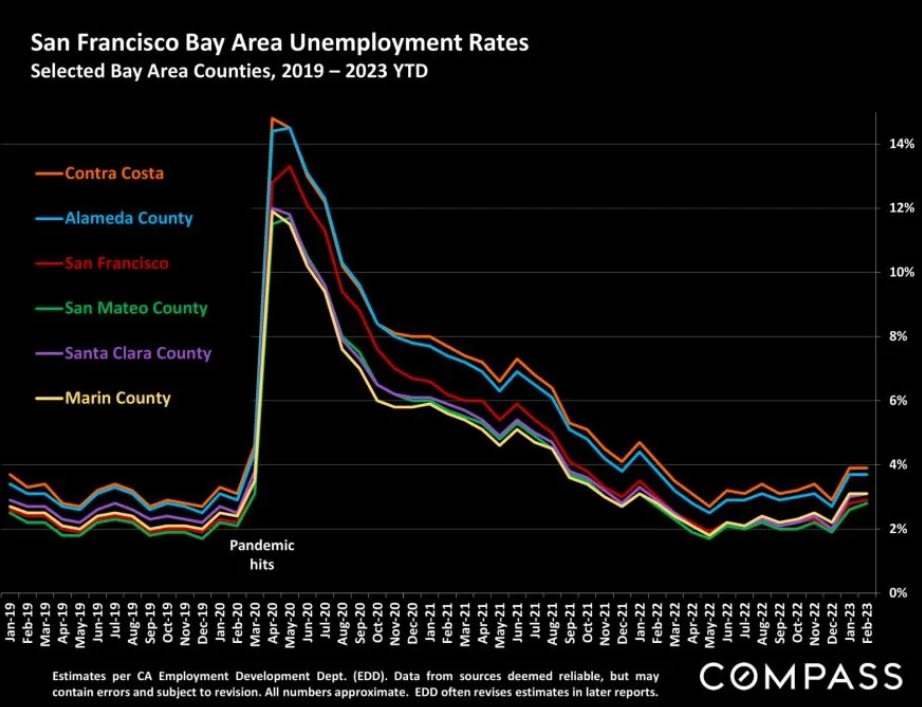

San Francisco Bay Area Unemployment Rates

Selected Bay Area Counties, 2019-2023 YTD

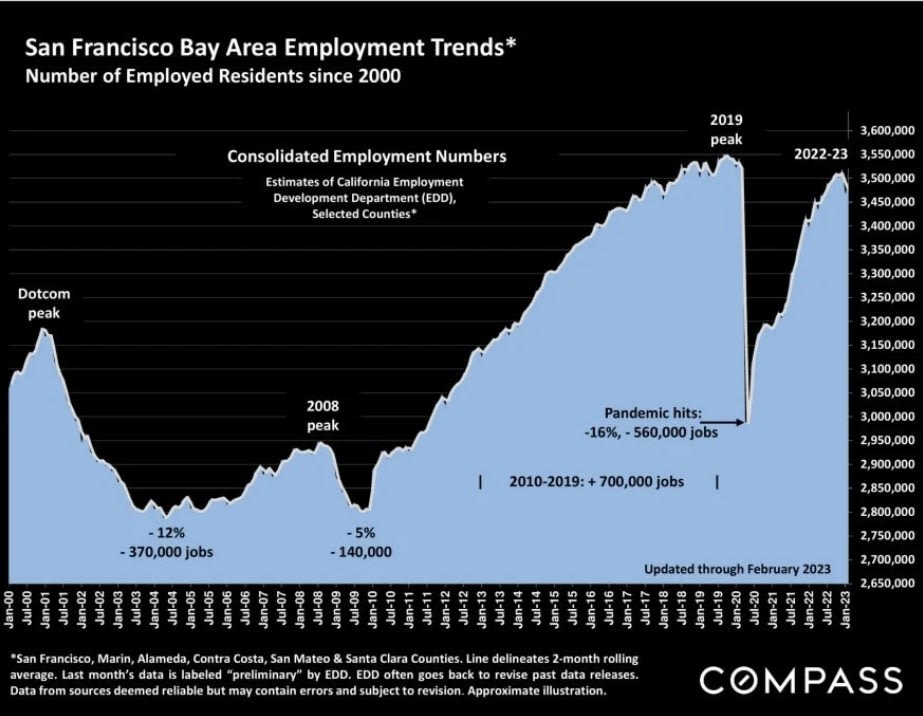

San Francisco Bay Area Employment Trends*

Number of Employed Residents since 2000

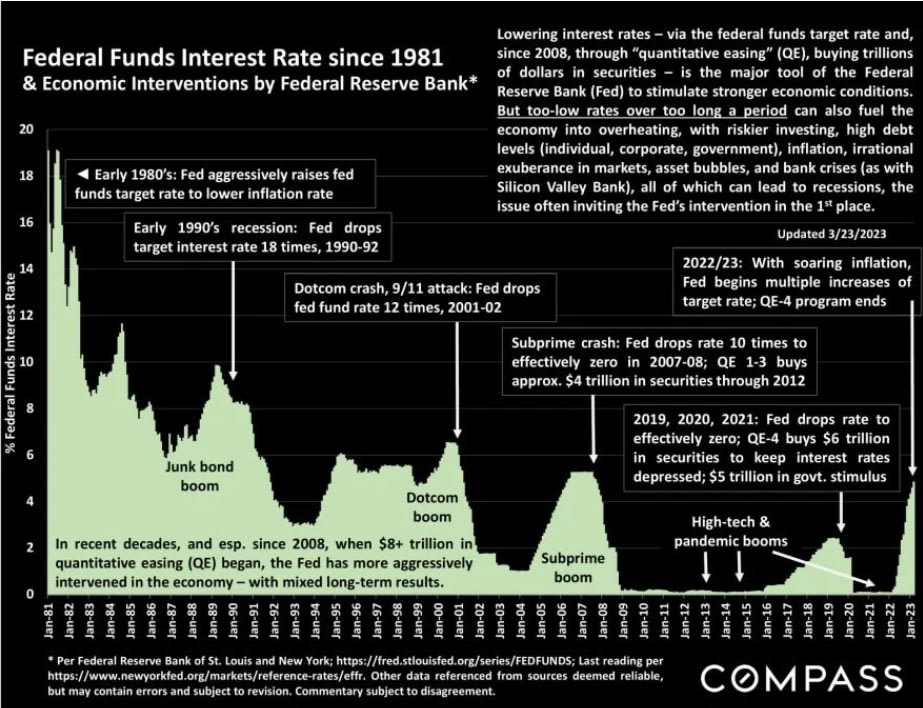

Federal Funds Interest Rate since 1981 & Economic Interventions by Federal Reserve Bank*

Lowering interest rates- via the federal funds target rate and, since 2008, through "quantitative easing" (QE), buying trillions of dollars in securities - is the major tool of the Federal Reserve Bank (Fed) to stimulate stronger economic conditions, But too-low rates over too long a period can also fuel the economy into overheating, with risker investing, high debt levels (individual, corporate, government), inflation, irrational exuberance in markets, asset bubbles and bank crises (as with Silicon Valley Bank), all of which can lead to recessions, the issue often inviting the Fed's intervention in the 1st place.

State Income Taxes as a Macroeconomic Factor

California has long ranked high in state income taxes (and housing cost), but the dramatic 2017 tax law changes to the maximum federal income tax deduction for state and local taxes (such as state income and property taxes) significantly exacerbated the negative financial effect for the state's high-earning residents. State tax rates have become an increasing factor in population migration and housing markets, especially with the post-pandemic movement to "work from home." Some of the states seeing the highest CA resident migration numbers, besides having no state income taxes, also host large high-tech industries.

Top Income Tax Rates

1.California 13.3%

2.Hawaii 11%

3. New Jersey 10.75%

4.Oregon 9.9%

5. Minnesota 9.85%

6.District of Columbia 8.95%

7.New York 8.82%

The details of minimum income, deductions, credits, exemptions and tax rate by income threshold vary by state.

"A comparison of 2020 tax rates compiled by the Tax Foundation ranks California as the top taxer with a 12.3% rate, unless you make more than $1 million. Then, you have to pay 13.3% as the top rate.

"Tax rates and rankings quoted from Intuit Turbo Tax: https://turbotax.intuit.com/tax-tips/fun-facts/states-with-the-highest-and-lowest-taxes/L6HPAVqSF.

Migration rankings per 2019 U.S. census figures.

All data herein from sources deemed reliable, but may contain errors and subject to revision. Interested parties should independently verify.

No State Income Tax

•Texas - highest CA resident migration numbers

•Nevada - 3rd highest CA migration

•Washington - 4th highest CA migration

•Florida - 7th highest CA migration

Arizona ranks 2nd for CA resident migration, with a maximum 2022 state income tax rate of 2.98% per the AZ Dept. of Revenue.

The top 8 states for 2022 population growth include Arizona, Nevada, Texas, Florida and Washington (per https://worldpopulationreview.com/state-rankings/fastest-growing-states)

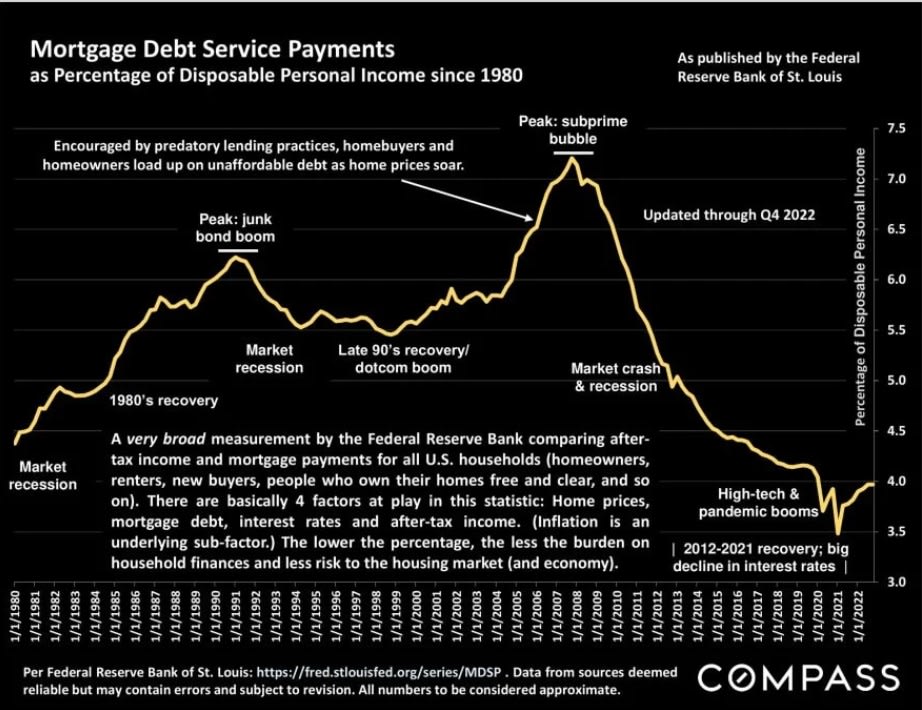

Mortgage Debt Service Payments

as Percentage of Disposable Personal Income since 1980

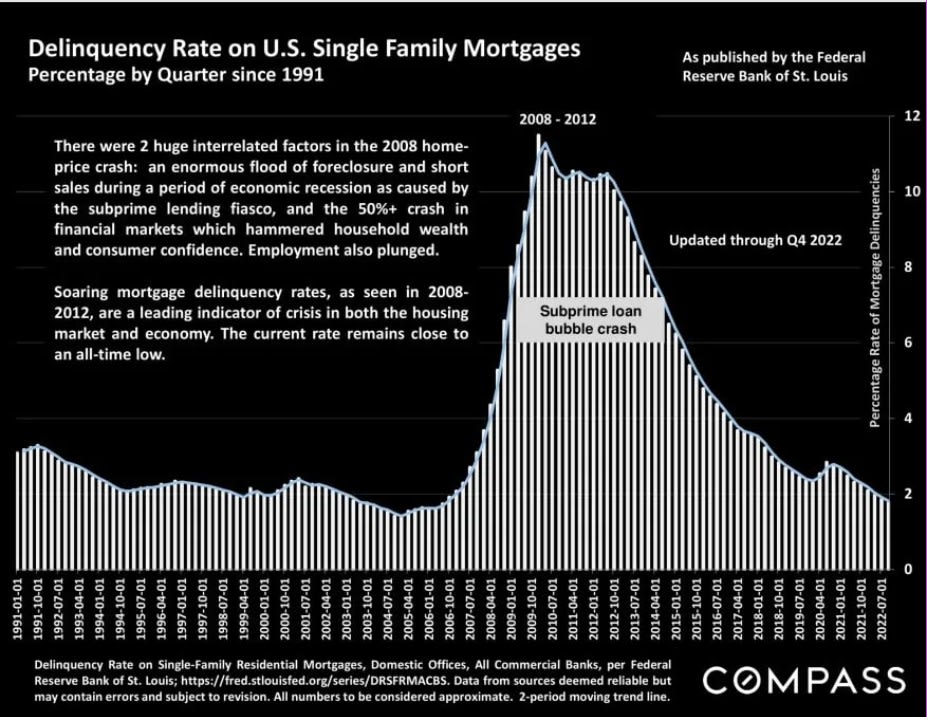

Delinquency Rate on U.S. Single Family Mortgages

Percentage by Quarter since 1991

There were 2 huge interrelated factors in the 2008 home-price crash: an enormous flood of foreclosure and short sales during a period of economic recession as caused by the subprime lending fiasco, and the 50%+ crash in financial markets which hammered household wealth and consumer confidence. Employment also plunged.

Soaring mortgage delinquency rates, as seen in 2008-2012, are a leading indicator of crisis in both the housing market and economy. The current rate remains close to an all-time low.

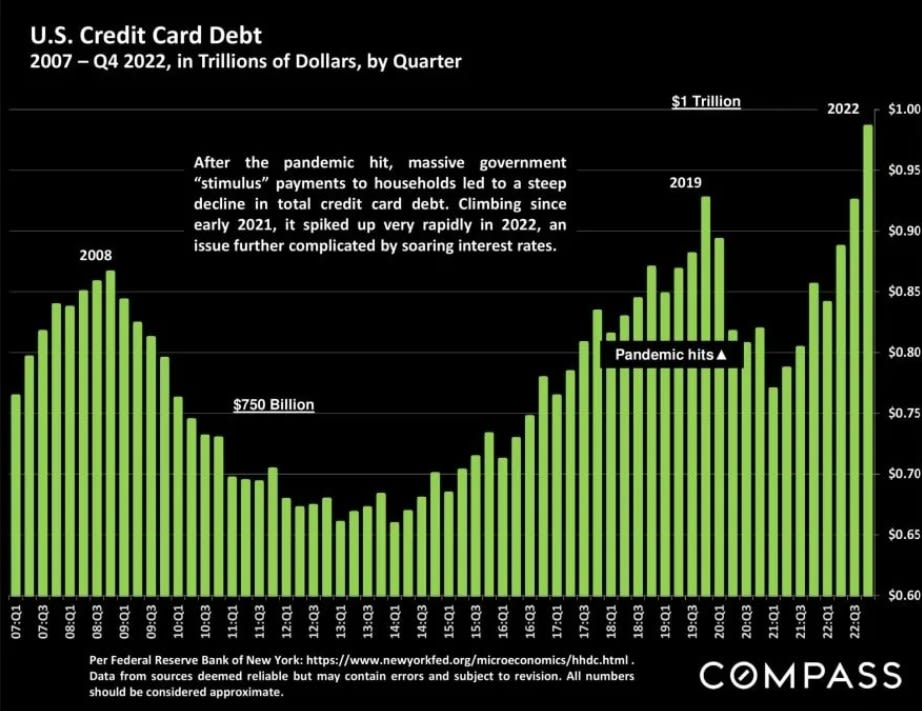

US. Credit Card Debt

2007 - Q4 2022, in Trillions of Dollars, by Quarter

After the pandemic hit, massive government "stimulus" payments to households led to a steep decline in total credit card debt. Climbing since early 2021, it spiked up very rapidly in 2022, an issue further complicated by soaring interest rates.

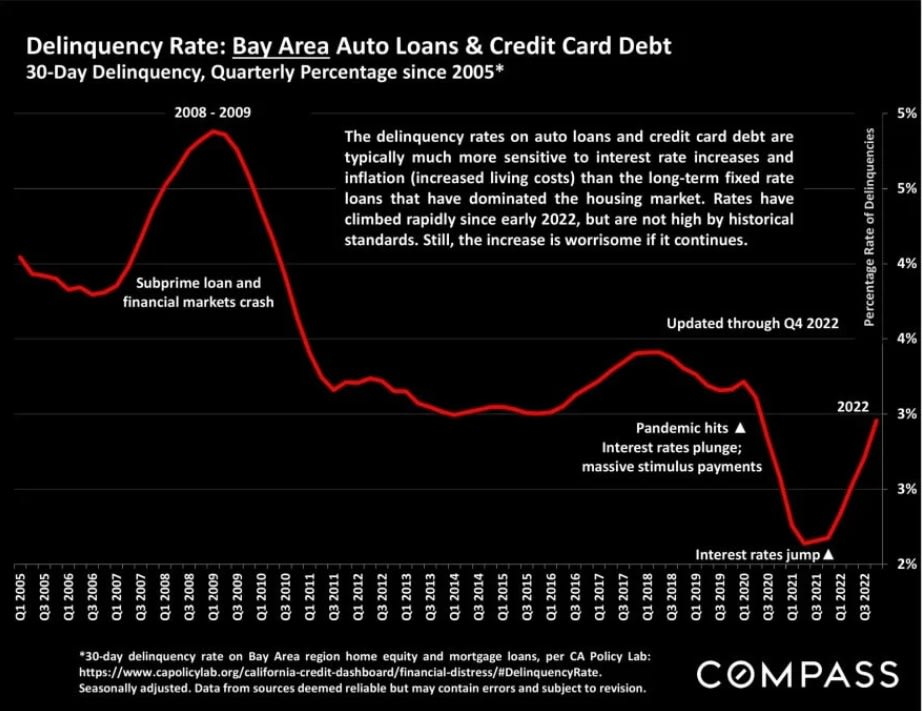

Delinquency Rate: Bay Area Auto Loans & Credit Card Debt

30-Day Delinquency, Quarterly Percentage since 2005*

The delinquency rates on auto loans and credit card debt are typically much more sensitive to interest rate increases and inflation (increased living costs) than the long-term fixed rate loans that have dominated the housing market. Rates have climbed rapidly since early 2022, but are not high by historical standards. Still, the increase is worrisome if it continues.

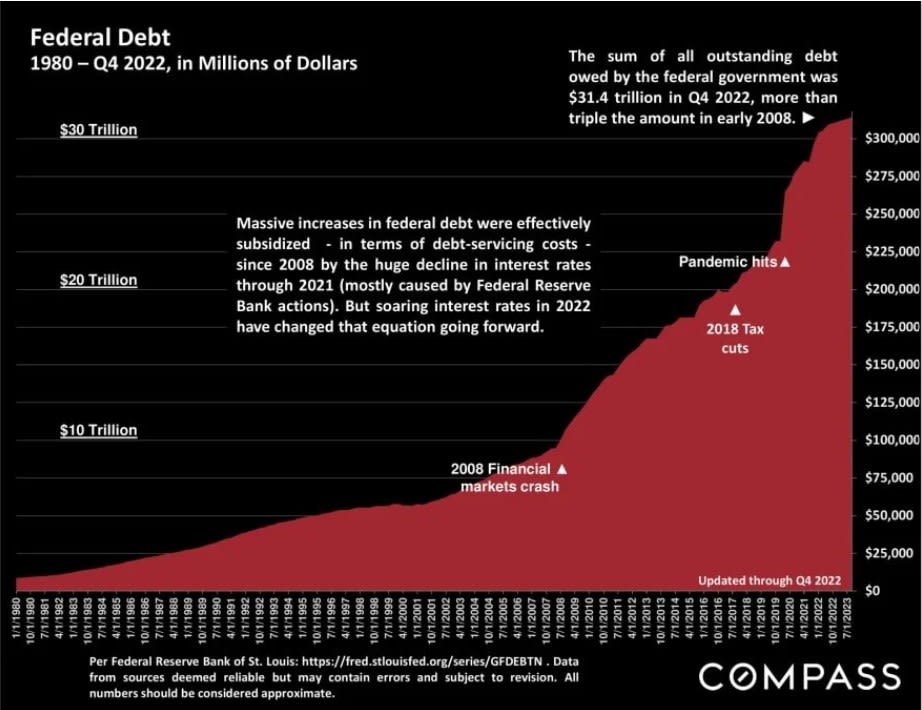

Federal Debt

1980- Q4 2022, in Millions of Dollars

The sum of all outstanding debt owed by the federal government was $31.4 trillion in Q4 2022, more than triple the amount in early 2008.

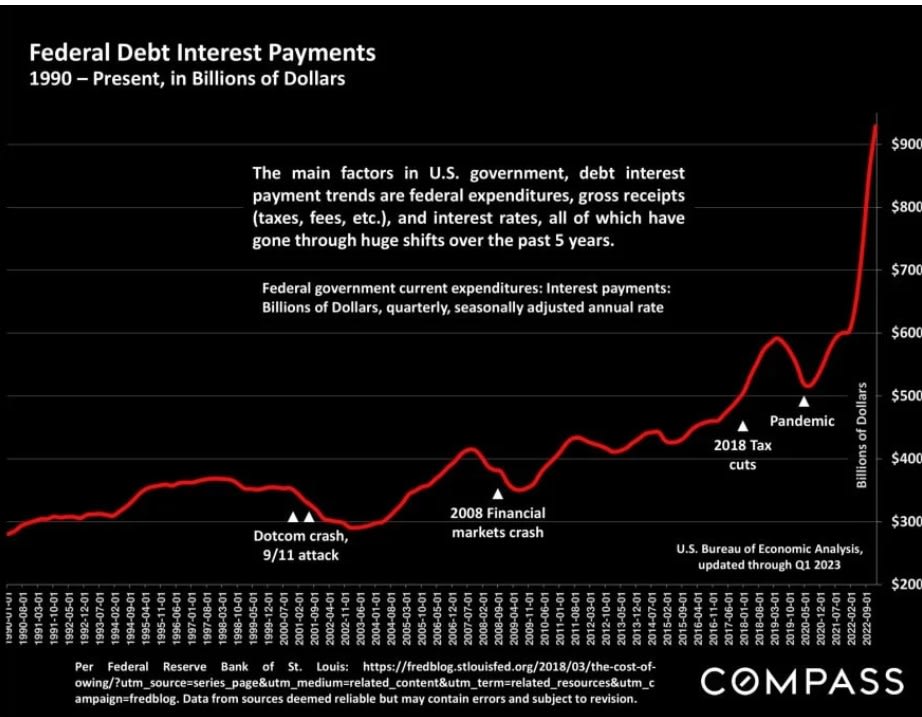

Federal Debt Interest Payments

1990 - Present , in Billion of Dollars

The main factors in U.S. government, debt interest payment trends are federal expenditures, gross receipts (taxes, fees, etc.) and interest rates, all of which have gone through huge shifts over the past 5 years.

Federal government current expenditures: Interest payments: Billions of Dollars, quarterly, seasonally adjusted annual rate

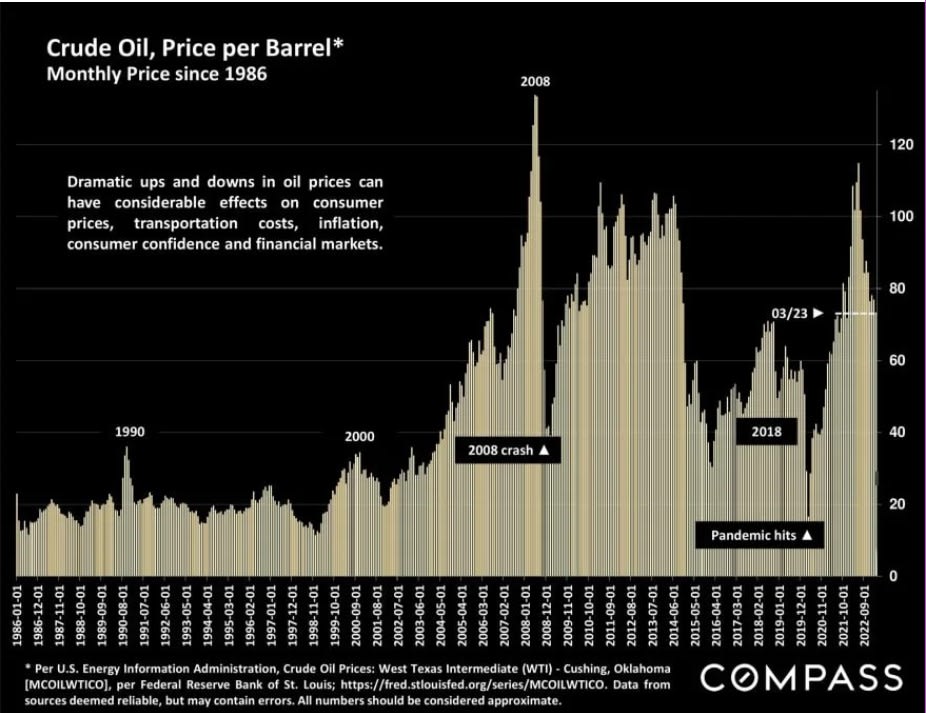

Crude Oil, Price per Barrel*

Monthly Price since 1986

Dramatic ups and downs in oil prices can have considerable effects on consumer prices, transportation costs, inflation, consumer confidence and financial markets.

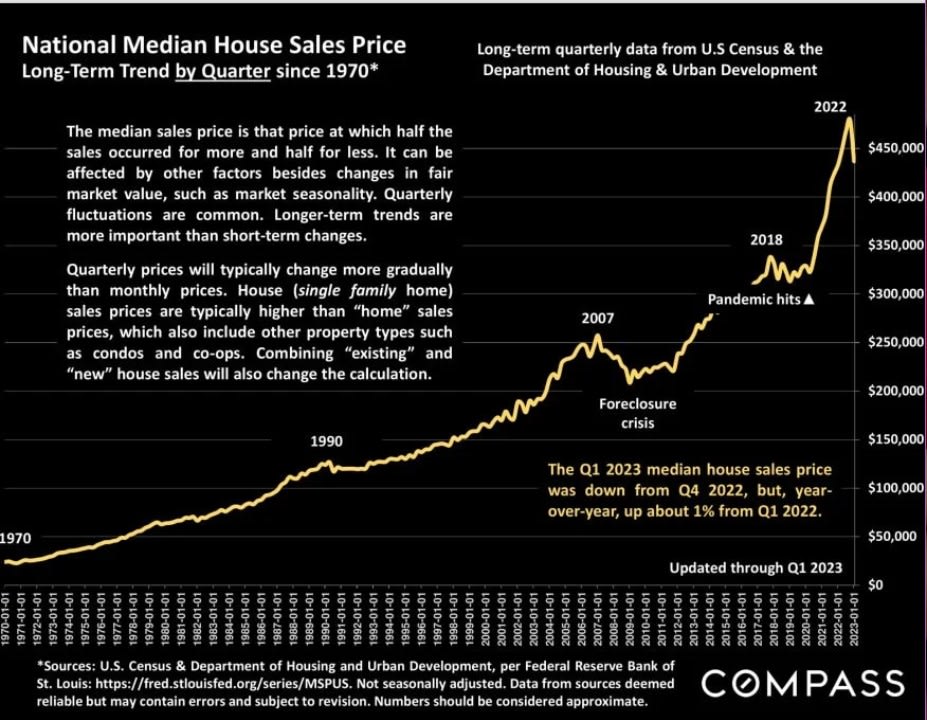

National Median House Sales Price

Long-Term Trend by Quarter since 1970*

The median sales price is that price at which half the sales occurred for more and half for less. It can be affected by other factors besides changes in fair market value, such as market seasonality. Quarterly fluctuations are common. Longer-term trends are more important than short-term changes.

Quarterly prices will typically change more gradually than monthly prices. House (single family home) sales prices are typically higher than "home" sales prices, which also include other property types such as condos and co-ops. Combining "existing" and "new" house sales will also change the calculation.

The Q1 2023 median house sales price was down from Q4 2022, but, year-over-year, up about 1% from Q1 2022.

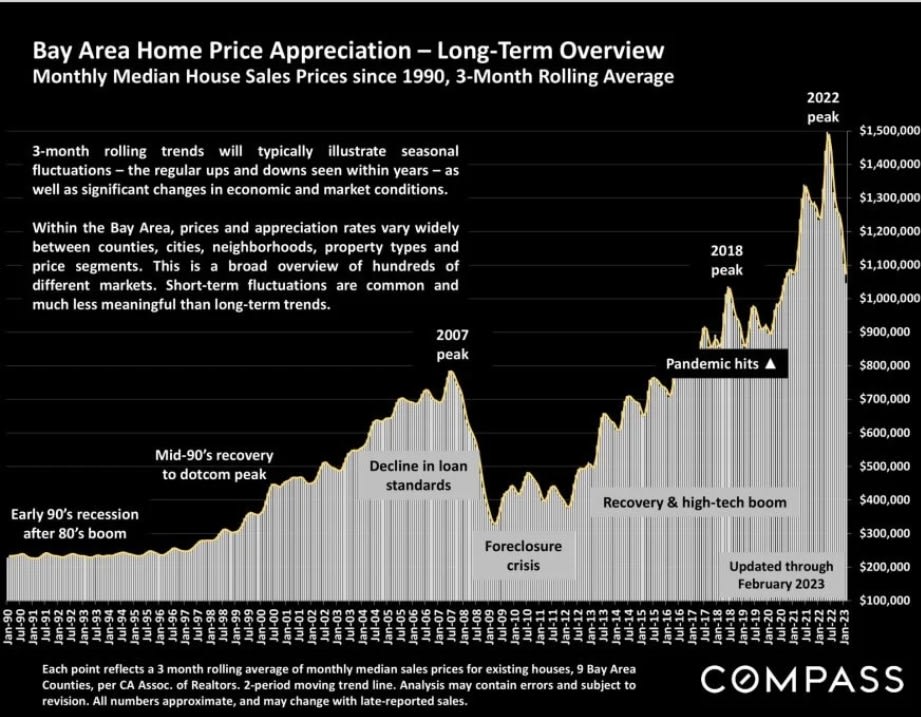

Bay Area Home Price Appreciation - Long-Term Overview

Monthly Median House Sales Prices since 1990, 3-Month Rolling Average

3-month rolling trends will typically illustrate seasonal fluctuations - the regular ups and downs seen within years - as well as significant changes in economic and market conditions.

Within the Bay Area, prices and appreciation rates vary widely between counties, cities, neighborhoods, property types and price segments. This is a broad overview of hundreds of different markets. Short-term fluctuations are common and much less meaningful than long-term trends.

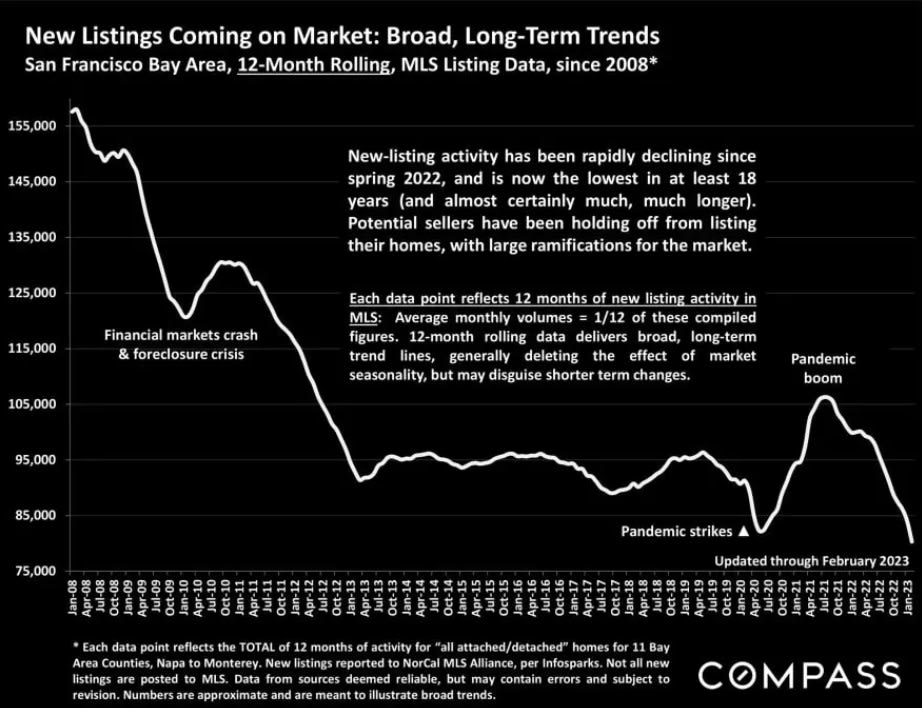

New Listings Coming on Market: Broad, Long-Term Trends

San Francisco Bay Area, 12- Month Rolling, MLS Listing Data, since 2008*

New-listing activity has been rapidly declining since spring 2022, and is now the lowest in at least 18 years (and almost certainly much, much longer). Potential sellers have been holding off from listing their homes, with large ramifications for the market.

Each data point reflects 12 months of new listing activity in MLS: Average monthly volumes = 1/12 of these compiled figures. 12-month rolling data delivers broad, long-term trend lines, generally deleting the effect of market seasonality, but may disguise shorter term changes.

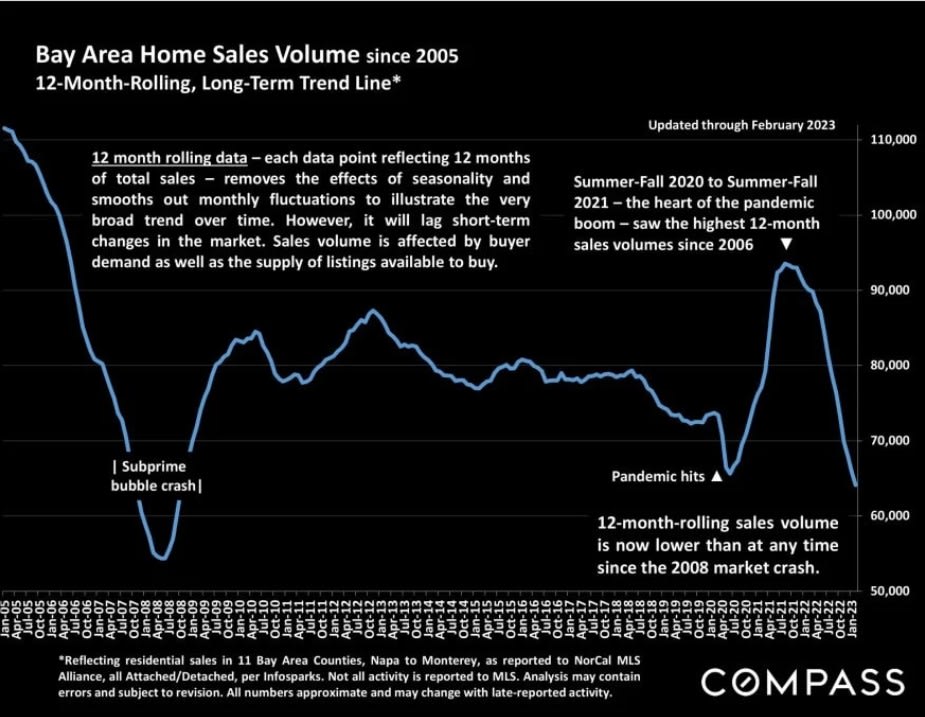

Bay Area Home Sales Volume since 2005

12-Month-Rolling, Long-Term Trend Line*

12 month rolling data - each data point reflecting 12 months of total sales - removes the effects of seasonality and smooths out monthly fluctuations to illustrate the very broad trend over time. However, it will lag short-term changes in the market. Sales volume is affected by buyer demand as well as the supply of listings available to buy.

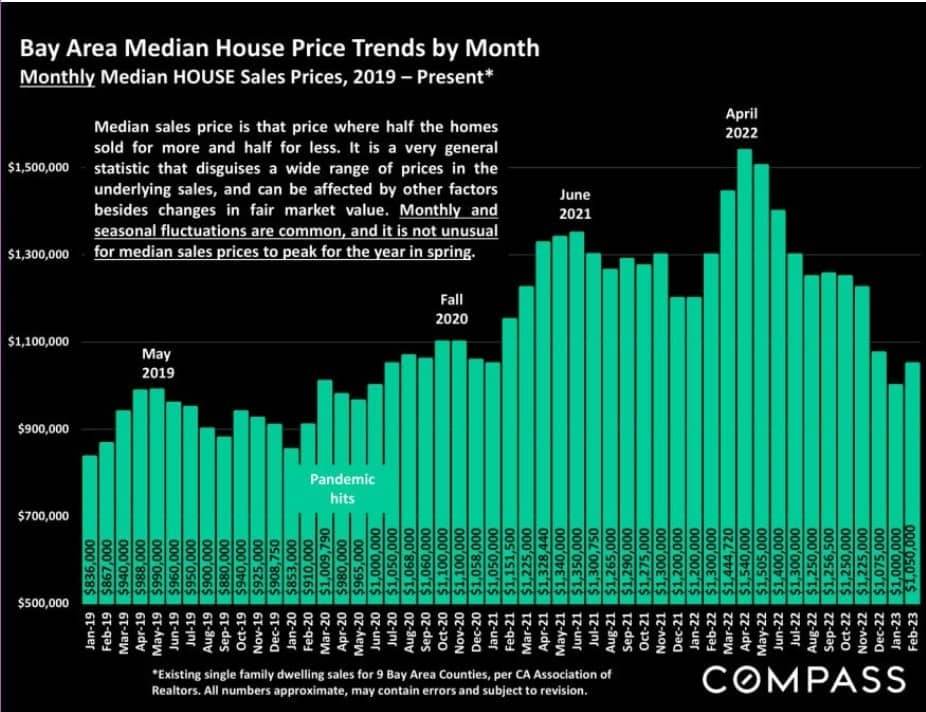

Bay Area Median House Price Trends by Month

Monthly Median HOUSE Sales Prices, 2019 - Present*

Median sales price is that price where half the homes sold for more and half for less. It is a very general statistic that disguises a wide range of prices in the underlying sales, and can be affected by other factors besides changes in fair market value. Monthly and seasonal fluctuations are common, and it is not unusual for median sales prices to peak for the year in spring.

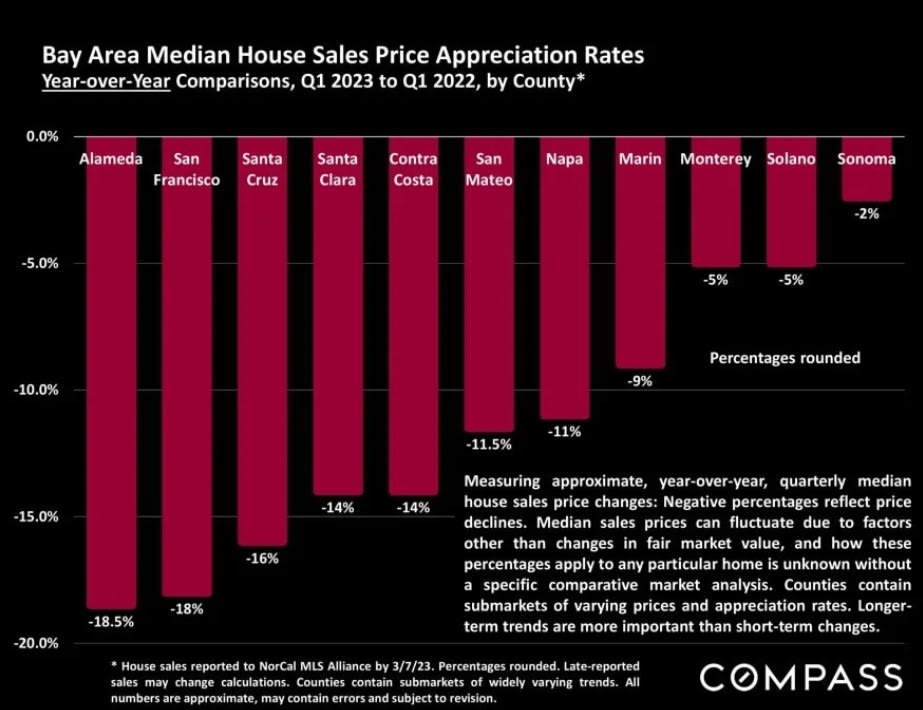

Bay Area Median House Sales Price Appreciation Rates

Year-over-Year Comparisons, Q1 2023 to Q1 2022, by County*

Measuring approximate, year-over-year, quarterly median -14% -14% house sales price changes: Negative percentages reflect price declines. Median sales prices can fluctuate due to factors other than changes in fair market value, and how these percentages apply to any particular home is unknown without a specific comparative market analysis. Counties contain submarkets of varying prices and appreciation rates. Longer-term trends are more important than short-term changes.

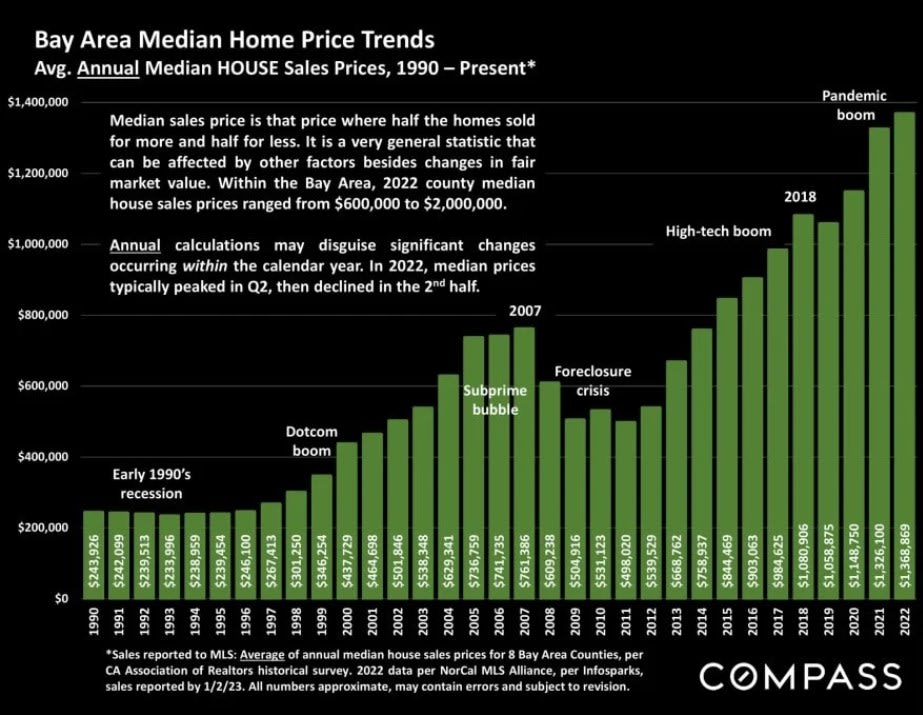

Bay Area Median Home Price Trends

Avg. Annual Median HOUSE Sales Prices, 1990 - Present*

Median sales price is that price where half the homes sold for more and half for less. It is a very general statistic that can be affected by other factors besides changes in fair market value. Within the Bay Area, 2022 county median house sales prices ranged from $600,000 to $2,000,000.

Annual calculations may disguise significant changes occurring within the calendar year. In 2022, median prices typically peaked in Q2, then declined in the 2nd half.

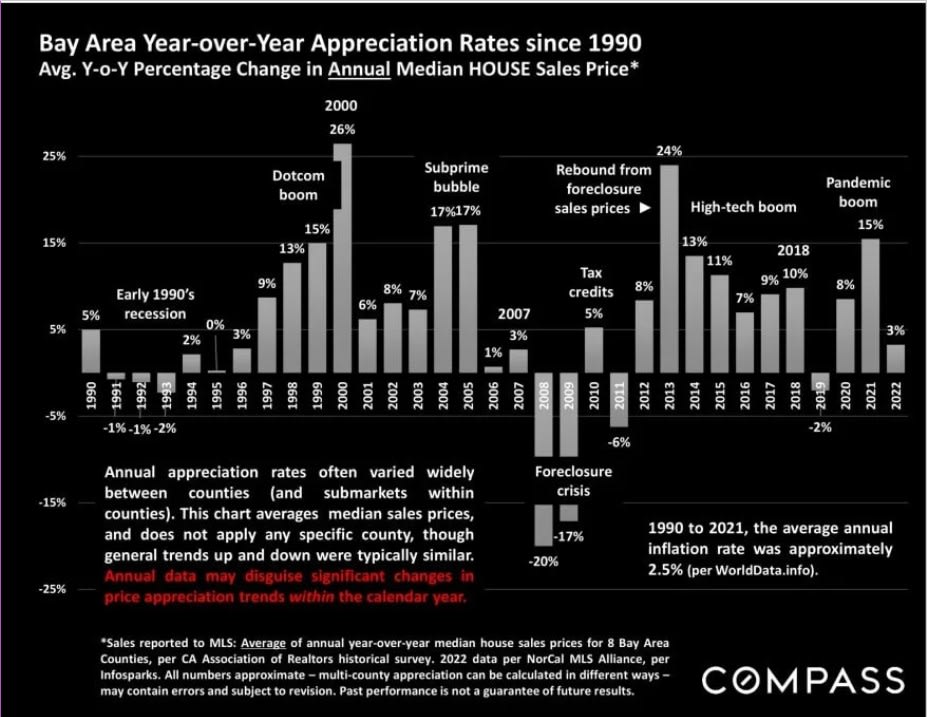

Bay Area Year-over-Year Appreciation Rates since 1990

Avg. Y-o-Y Percentage Change in Annual Median HOUSE Sales Price*

Annual appreciation rates often varied between counties widely (and submarkets counties). This chart averages within median sales prices, and does not apply any specific county, though general trends up and down were typically similar. Annual data may disguise significant changes in price appreciation trends within the calendar year.

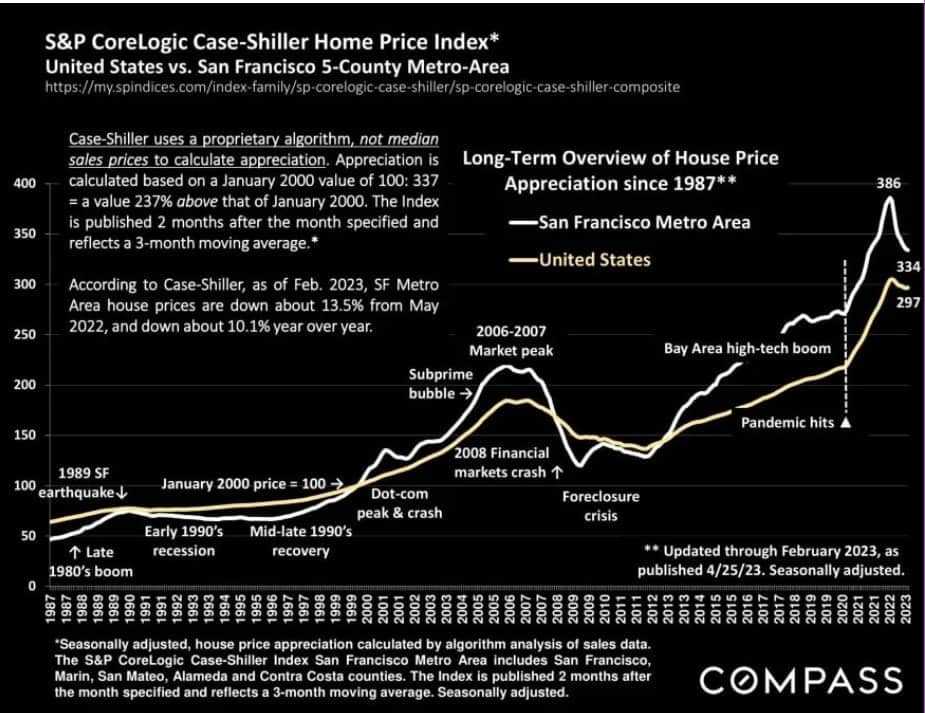

S&P CoreLogic Case-Shiller Home Price Index*

United States vs. San Francisco 5-County Metro Area

Case-Shiller uses a proprietary algorithm, not median sales prices to calculate appreciation. Appreciation is calculated based on a January 2000 value of 100: 337 = a value 237% above that of January 2000. The Index is published 2 months after the month specified and reflects a 3-month moving average.*

According to Case-Shiller, as of Feb. 2023, SF Metro Area house prices are down about 13.5% from May 2022, and down about 10.1% year over year.

Median House Sales Prices, Selected Metro Areas

Q1 2023 Median Sales Price & Year-over-Year % Price Change*

"Metro Areas" typically cover much larger regions - often multiple counties - than the cities they are named for, with wide variations

San Francisco Bay Area Home Price Appreciation Trends since 1990

The early 1990's recession, the dotcom boom, subprime bubble and crash, market recovery, high-tech boom - and pandemic.

Important notes and caveats regarding the context and methodology of this report are detailed on the last page. All calculations to be considered very approximate, good-faith estimates. How this report applies to any particular home is unknown without a specific comparative market analysis.

COMPASS San Francisco Bay Area Market Reports: https://www.BayAreaMarketReports.com

Statistics are generalities, essentially summaries of widely disparate data generated by dozens, hundreds or thousands of unique, individual sales occurring within different time periods. They are best seen not as precise measurements, but as broad, comparative indicators, with reasonable margins of error. Anomalous fluctuations in statistics are not uncommon, especially in smaller, expensive market segments. Last period data should be considered estimates that may change with late-reported data. Different analytics programs sometimes define statistics - such as "active listings," "days on market," and "months supply of inventory" - differently: what is most meaningful are not specific calculations but the trends they illustrate. Most listing and sales data derives from the local or regional multi-listing service (MLS) of the area specified in the analysis, but not all listings or sales are reported to MLS and these won't be reflected in the data. "Homes" signifies real-property, single-household housing units: houses, condos, co-ops, townhouses, duets and TICs (but not mobile homes), as applicable to each market. City/town names refer specifically to the named cities and towns, or their MLS areas, unless otherwise delineated. Multi-county metro areas will be specified as such. Data from sources deemed reliable, but may contain errors and subject to revision. All numbers to be considered approximate.

Many aspects of value cannot be adequately reflected in median and average statistics: curb appeal, age, condition, amenities, views, lot size, quality of outdoor space, "bonus" rooms, additional parking, quality of location within the neighborhood, and so on. How any of these statistics apply to any particular home is unknown without a specific comparative market analysis.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.